One of many extra attention-grabbing long-term sensible advantages of the expertise and idea behind decentralized autonomous organizations is that DAOs enable us to in a short time prototype and experiment with a facet of our social interactions that’s to date arguably falling behind our fast developments in data and social expertise elsewhere: organizational governance. Though our fashionable communications expertise is drastically augmenting people’ naturally restricted means to each work together and collect and course of data, the governance processes we now have at this time are nonetheless depending on what could now be seen as centralized crutches and arbitrary distinctions resembling “member”, “worker”, “buyer” and “investor” – options that have been arguably initially mandatory due to the inherent difficulties of managing massive numbers of individuals up up to now, however maybe not. Now, it might be doable to create techniques which might be extra fluid and generalized that make the most of the total energy legislation curve of individuals’s means and want to contribute. There are a selection of latest governance fashions that attempt to make the most of our new instruments to enhance transparency and effectivity, together with liquid democracy and holacracy; the one which I’ll focus on and dissect at this time is futarchy.

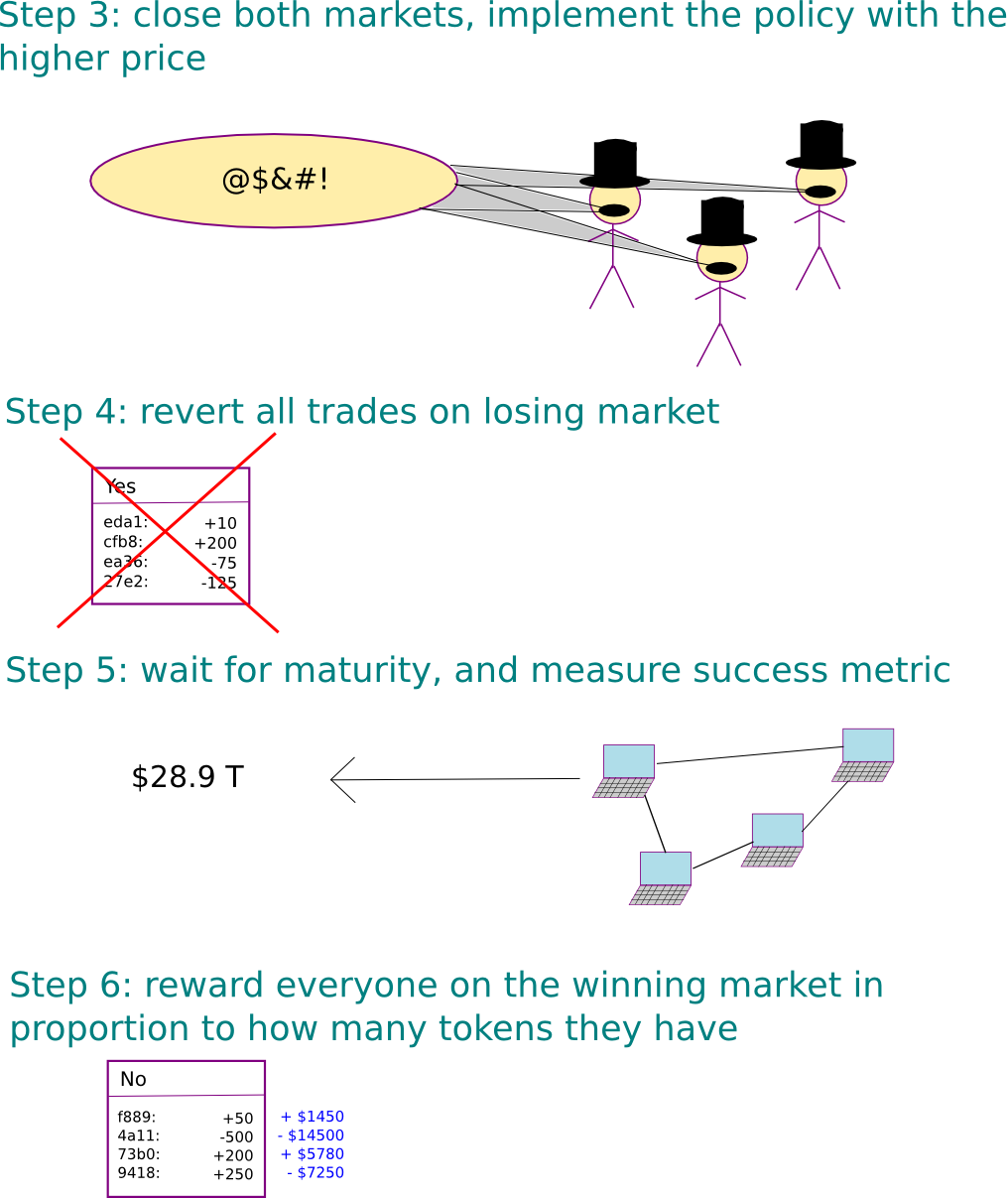

The concept behind futarchy was initially proposed by economist Robin Hanson as a futuristic type of authorities, following the slogan: vote values, however guess beliefs. Below this technique, people would vote not on whether or not or to not implement specific insurance policies, however relatively on a metric to find out how nicely their nation (or charity or firm) is doing, after which prediction markets can be used to choose the insurance policies that finest optimize the metric. Given a proposal to approve or reject, two prediction markets can be created every containing one asset, one market similar to acceptance of the measure and one to rejection. If the proposal is accepted, then all trades on the rejection market can be reverted, however on the acceptance market after a while everybody can be paid some quantity per token primarily based on the futarchy’s chosen success metric, and vice versa if the proposal is rejected. The market is allowed to run for a while, after which on the finish the coverage with the upper common token value is chosen.

Our curiosity in futarchy, as defined above, is in a barely completely different kind and use case of futarchy, governing decentralized autonomous organizations and cryptographic protocols; nevertheless, I’m presenting the usage of futarchy in a nationwide authorities first as a result of it’s a extra acquainted context. So to see how futarchy works, let’s undergo an instance.

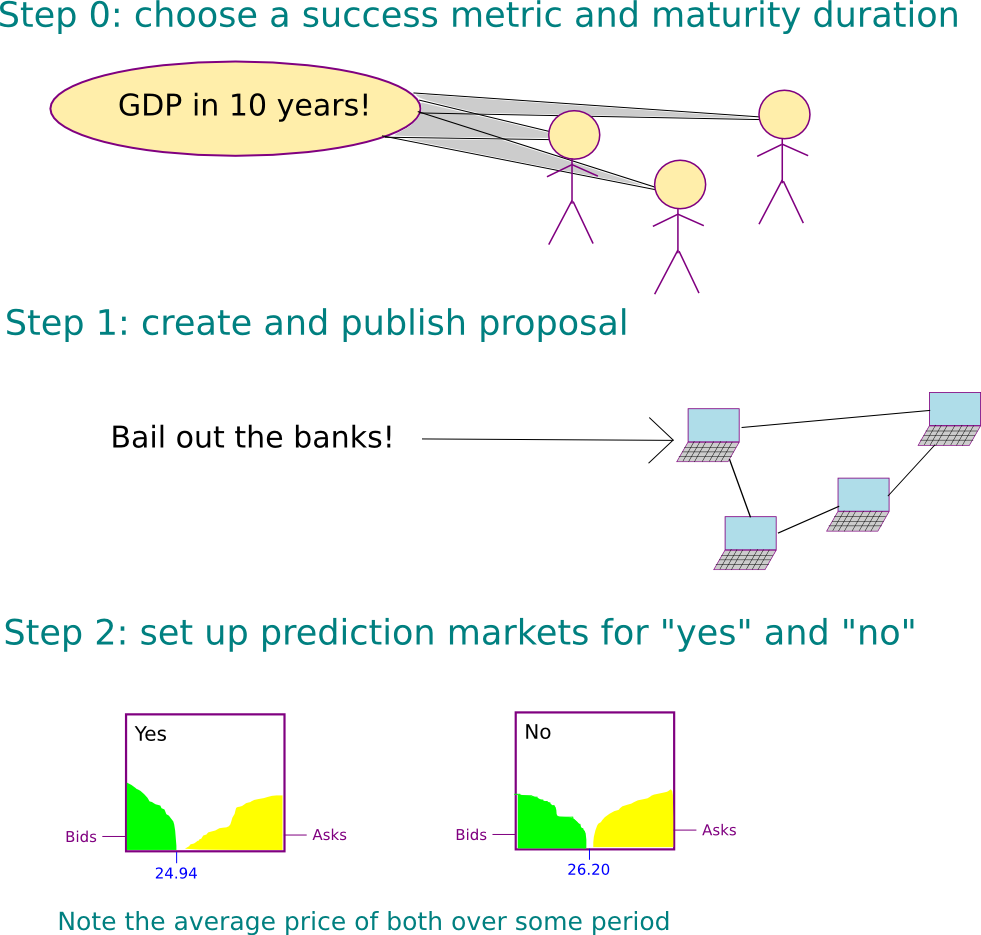

Suppose that the success metric chosen is GDP in trillions of {dollars}, with a time delay of ten years, and there exists a proposed coverage: “bail out the banks”. Two property are launched, every of which guarantees to pay $1 per token per trillion {dollars} of GDP after ten years. The markets could be allowed to run for 2 weeks, throughout which the “sure” token fetches a median value of $24.94 (that means that the market thinks that the GDP after ten years might be $24.94 trillion) and the “no” token fetches a median value of $26.20. The banks are usually not bailed out. All trades on the “sure” market are reverted, and after ten years everybody holding the asset on the “no” market will get $26.20 apiece.

Usually, the property in a futarchy are zero-supply property, just like Ripple IOUs or BitAssets. Which means that the one approach the tokens could be created is thru a derivatives market; people can place orders to purchase or promote tokens, and if two orders match the tokens are transferred from the customer to the vendor in trade for USD. It is doable to promote tokens even in case you would not have them; the one requirement in that case is that the vendor should put down some quantity of collateral to cowl the eventual destructive reward. An essential consequence of the zero-supply property is that as a result of the optimistic and destructive portions, and due to this fact rewards cancel one another out, barring communication and consensus prices the market is definitely free to function.

The Argument For

Futarchy has change into a controversial topic for the reason that thought was initially proposed. The theoretical advantages are quite a few. To begin with, futarchy fixes the “voter apathy” and “rational irrationality” downside in democracy, the place people would not have sufficient incentive to even study doubtlessly dangerous insurance policies as a result of the likelihood that their vote will have an impact is insignificant (estimated at 1 in 10 million for a US authorities nationwide election); in futarchy, in case you have or get hold of data that others would not have, you’ll be able to personally considerably revenue from it, and if you’re unsuitable you lose cash. Primarily, you’re actually placing your cash the place your mouth is.

Second, over time the market has an evolutionary strain to get higher; the people who’re unhealthy at predicting the result of insurance policies will lose cash, and so their affect available on the market will lower, whereas the people who’re good at predicting the result of insurance policies will see their cash and affect available on the market enhance. Be aware that that is primarily the very same mechanic by way of which economists argue that conventional capitalism works at optimizing the manufacturing of personal items, besides on this case it additionally applies to frequent and public items.

Third, one may argue that futarchy reduces doubtlessly irrational social influences to the governance course of. It’s a well-known indisputable fact that, not less than within the twentieth century, the taller presidential candidate has been more likely to win the election (apparently, the reverse bias existed pre-1920; a doable speculation is that the switchover was brought on by the contemporaneous rise of tv), and there may be the well-known story about voters choosing George Bush as a result of he was the president “they might relatively have a beer with“. In futarchy, the participatory governance course of will maybe encourage focusing extra purely on proposals relatively than personalities, and the first exercise is probably the most introverted and unsocial affair conceivable: poring over fashions, statistical analyses and buying and selling charts.

A market you’ll relatively have a beer with

The system additionally elegantly combines public participation {and professional} evaluation. Many individuals decry democracy as a descent to mediocrity and demagoguery, and like selections to be made by expert technocratic specialists. Futarchy, if it really works, permits particular person specialists and even whole evaluation companies to make particular person investigations and analyses, incorporate their findings into the choice by shopping for and promoting available on the market, and make a revenue from the differential in data between themselves and the general public – kind of like an information-theoretic hydroelectric dam or osmosis-based energy plant. However in contrast to extra rigidly organized and bureaucratic technocracies with a pointy distinction between member and non-member, futarchies enable anybody to take part, arrange their very own evaluation agency, and if their analyses are profitable finally rise to the highest – precisely the type of generalization and fluidity we’re in search of.

The Argument Towards

The opposition to futarchy is most well-summarized in two posts, one by Mencius Moldbug and the different by Paul Hewitt. Each posts are lengthy, taking over 1000’s of phrases, however the common classes of opposition could be summarized as follows:

- A single highly effective entity or coalition wishing to see a selected consequence can proceed shopping for “sure” tokens available on the market and short-selling “no” tokens with a purpose to push the token costs in its favor.

- Markets on the whole are recognized to be risky, and this occurs to a big extent as a result of markets are “self-referential” – ie. they consist largely of individuals shopping for as a result of they see others shopping for, and so they don’t seem to be good aggregators of precise data. This impact is especially harmful as a result of it may be exploited by market manipulation.

- The estimated impact of a single coverage on a world metric is way smaller than the “noise” of uncertainty in what the worth of the metric goes to be whatever the coverage being carried out, particularly in the long run. Which means that the prediction market’s outcomes could show to be wildly uncorrellated to the precise delta that the person insurance policies will find yourself having.

- Human values are complicated, and it’s exhausting to compress them into one numerical metric; actually, there could also be simply as many disagreements about what the metric ought to be as there are disagreements about coverage now. Moreover, a malicious entity that in present democracy would attempt to foyer by way of a dangerous coverage may as a substitute have the ability to cheat the futarchy by lobbying in an addition to the metric that’s recognized to very extremely correllate with the coverage.

- A prediction market is zero-sum; therefore, as a result of participation has assured nonzero communication prices, it’s irrational to take part. Thus, participation will find yourself fairly low, so there is not going to be sufficient market depth to permit specialists and evaluation companies to sufficiently revenue from the method of gathering data.

On the primary argument, this video debate between Robin Hanson and Mencius Moldbug, with David Friedman (Milton’s son) later chiming in, is maybe one of the best useful resource. The argument made by Hanson and Friedman is that the presence of a corporation doing such a factor efficiently would result in a market the place the costs for the “sure” and “no” tokens don’t really replicate the market’s finest information, presenting an enormous profit-earning alternative for individuals to place themselves on the alternative aspect of the tried manipulation and thereby transfer the worth again nearer to the right equilibrium. So as to give time for this to occur, the worth utilized in figuring out which coverage to take is taken as a median over some time period, not at one immediate. So long as the market energy of individuals prepared to earn a revenue by counteracting manipulation exceeds the market energy of the manipulator, the trustworthy members will win and extract a big amount of funds from the manipulator within the course of. Primarily, for Hanson and Friedman, sabotaging a futarchy requires a 51% assault.

The most typical rebuttal to this argument, made extra eloquently by Hewitt, is the “self-referential” property of markets talked about above. If the worth for “trillions of US GDP in ten years if we bail out the banks” begins off $24.94, and the worth for “trillions of US GDP in ten years if we do not bail out the banks” begins off $26.20, however then in the future the 2 cross over to $27.3 for sure and $25.1 for no, would individuals really know that the values are off and begin making trades to compensate, or would they merely take the brand new costs as an indicator of what the market thinks and settle for and even reinforce them, as is commonly theorized to occur in speculative bubbles?

Self-reference

There’s really one cause to be optimistic right here. Conventional markets could maybe be typically self-referential, and cryptocurrency markets particularly so as a result of they haven’t any intrinsic worth (ie. the one supply of their worth is their worth), however the self-reference occurs partially for a special cause than merely buyers following one another like lemmings. The mechanism is as follows. Suppose that an organization is occupied with elevating funds by way of share issuance, and presently has one million shares valued at $400, so a market cap of $400 million; it’s prepared to dilute its holders with a ten% enlargement. Thus, it may possibly increase $40 million. The market cap of the corporate is meant to focus on the overall quantity of dividends that the corporate will ever pay out, with future dividends appropriately discounted by some rate of interest; therefore, if the worth is secure, it implies that the market expects the corporate to finally launch the equal of $400 million in complete dividends in current worth.

Now, suppose the corporate’s share value doubles for some cause. The corporate can now increase $80 million, permitting it to do twice as a lot. Often, capital expenditure has diminishing returns, however not all the time; it might occur that with the additional $40 million capital the corporate will have the ability to earn twice as a lot revenue, so the brand new share value might be completely justified – though the reason for the bounce from $400 to $800 could have been manipulation or random noise. Bitcoin has this impact in an particularly pronounced approach; when the worth goes up, all Bitcoin customers get richer, permitting them to construct extra companies, justifying the upper value degree. The dearth of intrinsic worth for Bitcoin implies that the self-referential impact is the one impact having affect on the worth.

Prediction markets would not have this property in any respect. Except for the prediction market itself, there isn’t a believable mechanism by which the worth of the “sure” token on a prediction market can have any affect on the GDP of the US in ten years. Therefore, the one impact by which self-reference can occur is the “everybody follows everybody else’s judgement” impact. Nonetheless, the extent of this impact is debatable; maybe due to the very recognition that the impact exists, there may be now a longtime tradition of good contrarianism in funding, and politics is actually an space the place persons are prepared to maintain to unorthodox views. Moreover, in a futarchy, the related factor isn’t how excessive particular person costs are, however which one of many two is increased; if you’re sure that bailouts are unhealthy, however you see the yes-bailout value is now $2.2 increased for some cause, that one thing is unsuitable so, in principle, you may have the ability to fairly reliably revenue from that.

Absolutes and differentials

That is the place we get to the crux of the actual downside: it is not clear how one can. Think about a extra excessive case than the sure/no bailouts choice: an organization utilizing a futarchy to find out how a lot to pay their CEO. There have been research suggesting that ultra-high-salary CEOs really don’t enhance firm efficiency – actually, a lot the alternative. So as to repair this downside, why not use the ability of futarchy and the market resolve how a lot worth the CEO actually supplies? Have a prediction marketplace for the corporate’s efficiency if the CEO stays on, and if the CEO jumps off, and take the CEO’s wage as a normal share of the distinction. We will do the identical even for lower-ranking executives and if futarchy finally ends up being magically good even the lowliest worker.

Now, suppose that you simply, as an analyst, predict that an organization utilizing such a scheme can have a share value of $7.20 in twelve months if the CEO stays on, with a 95% confidence interval of $2.50 (ie. you are 95% positive the worth might be between $4.70 and $9.70). You additionally predict that the CEO’s profit to the share value is $0.08; the 95% confidence interval that you’ve got right here is from $0.03 to $0.13. That is fairly life like; usually errors in measuring a variable are proportional to the worth of that variable, so the vary on the CEO might be a lot decrease. Now suppose that the prediction market has the token value of $7.70 if the CEO stays on and $7.40 in the event that they go away; briefly, the market thinks the CEO is a rockstar, however you disagree. However how do you profit from this?

The preliminary intuition is to purchase “no” shares and short-sell “sure” shares. However what number of of every? You may suppose “the identical variety of every, to stability issues out”, however the issue is that the prospect the CEO will stay on the job is way increased than 50%. Therefore, the “no” trades will most likely all be reverted and the “sure” trades is not going to, so alongside shorting the CEO what you’re additionally doing is taking a a lot bigger threat shorting the corporate. For those who knew the share change, then you might stability out the quick and lengthy purchases such that on web your publicity to unrelated volatility is zero; nevertheless, since you do not, the risk-to-reward ratio may be very excessive (and even in case you did, you’ll nonetheless be uncovered to the variance of the corporate’s world volatility; you simply wouldn’t be biased in any specific route).

From this, what we are able to surmise is that futarchy is prone to work nicely for large-scale selections, however a lot much less nicely for finer-grained duties. Therefore, a hybrid system may go higher, the place a futarchy decides on a political occasion each few months and that political occasion makes selections. This appears like giving complete management to at least one occasion, nevertheless it’s not; notice that if the market is afraid of one-party management then events may voluntarily construction themselves to be composed of a number of teams with competing ideologies and the market would like such mixtures; actually, we may have a system the place politicians enroll as people and anybody from the general public can submit a mixture of politicians to elect into parliament and the market would decide over all mixtures (though this may have the weak spot that it’s as soon as once more extra personality-driven).

Futarchy and Protocols and DAOs

The entire above was discussing futarchy primarily as a political system for managing authorities, and to a lesser extent firms and nonprofits. In authorities, if we apply futarchy to particular person legal guidelines, particularly ones with comparatively small impact like “scale back the length of patents from 20 years to 18 years”, we run into lots of the points that we described above. Moreover, the fourth argument in opposition to futarchy talked about above, the complexity of values, is a selected sore level, since as described above a considerable portion of political disagreement is exactly when it comes to the query of what the right values are. Between these issues, and political slowness on the whole, it appears unlikely that futarchy might be carried out on a nationwide scale any time quickly. Certainly, it has not even actually been tried for companies. Now, nevertheless, there may be a completely new class of entities for which futarchy could be significantly better suited, and the place it might lastly shine: DAOs.

To see how futarchy for DAOs may work, allow us to merely describe how a doable protocol would run on high of Ethereum:

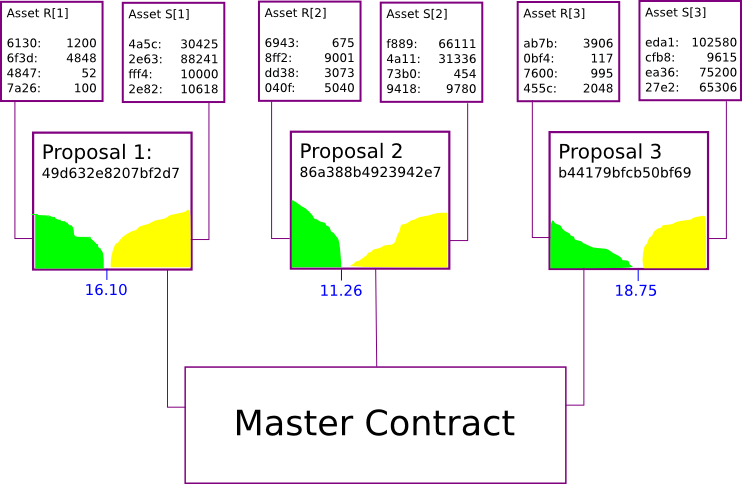

- Each spherical, T new DAO-tokens are issued. Firstly of a spherical, anybody has the power to make a proposal for the way these cash ought to be distributed. We will simplify and say {that a} “proposal” merely consists of “ship cash to this handle”; the precise plan for the way that cash can be spent can be communicated on some higher-level channel like a discussion board, and trust-free proposals may very well be made by sending to a contract. Suppose that n such proposals, P[1] … P[n], are made.

- The DAO generates n pairs of property, R[i] and S[i], and randomly distributes the T items of every sort of token in some trend (eg. to miners, to DAO token holders, in keeping with a components itself decided by way of prior futarchy, and so forth). The DAO additionally supplies n markets, the place market M[i] permits commerce between R[i] and S[i].

- The DAO watches the common value of S[i] denominated in R[i] for all markets, and lets the markets run for b blocks (eg. 2 weeks). On the finish of the interval, if market M[k] has the very best common value, then coverage P[k] is chosen, and the subsequent interval begins.

- At that time, tokens R[j] and S[j] for j != okay change into nugatory. Token R[k] is value m items of some exterior reference asset (eg. ETH for a futarchy on high of Ethereum), and token S[k] is value z DAO tokens, the place a great worth for z could be 0.1 and m self-adjusts to maintain expenditures cheap. Be aware that for this to work the DAO would want to additionally promote its personal tokens for the exterior reference asset, requiring one other allocation; maybe m ought to be focused so the token expenditure to buy the required ether is zT.

Primarily, what this protocol is doing is implementing a futarchy which is making an attempt to optimize for the token’s value. Now, let’s take a look at a number of the variations between this sort of futarchy and futarchy-for-government.

First, the futarchy right here is making solely a really restricted type of choice: to whom to assign the T tokens which might be generated in every spherical. This alone makes the futarchy right here a lot “safer”. A futarchy-as-government, particularly if unrestrained, has the potential to run into severe surprising points when mixed with the fragility-of-value downside: suppose that we agree that GDP per capita, even perhaps with some offsets for well being and setting, is one of the best worth perform to have. In that case, a coverage that kills off the 99.9% of the inhabitants that aren’t super-rich would win. If we choose plain GDP, then a coverage may win that extraordinarily closely subsidizes people and companies from outdoors relocating themselves to be contained in the nation, maybe utilizing a 99% one-time capital tax to pay for a subsidy. In fact, in actuality, futarchies would patch the worth perform and make a brand new invoice to reverse the unique invoice earlier than implementing any such apparent egregious instances, but when such reversions change into too commonplace then the futarchy primarily degrades into being a conventional democracy. Right here, the worst that might occur is for all of the N tokens in a selected spherical to go to somebody who will squander them.

Second, notice the completely different mechanism for the way the markets work. In conventional futarchy, we now have a zero-total-supply asset that’s traded into existence on a derivatives market, and trades on the shedding market are reverted. Right here, we problem positive-supply property, and the best way that trades are reverted is that all the issuance course of is actually reverted; each property on all shedding markets change into value zero.

The most important distinction right here is the query of whether or not or not individuals will take part. Allow us to return to the sooner criticism of futarchy, that it’s irrational to take part as a result of it’s a zero-sum sport. That is considerably of a paradox. When you have some inside data, then you definitely may suppose that it’s rational to take part, as a result of one thing that different individuals do not and thus your expectation of the eventual settlement value of the property is completely different from the market’s; therefore, you need to have the ability to revenue from the distinction. Alternatively, if everybody thinks this manner, then even some individuals with inside data will lose out; therefore, the right criterion for collaborating is one thing like “you need to take part in case you suppose you will have higher inside data than everybody else collaborating”. But when everybody thinks this manner then the equilibrium might be that nobody participates.

Right here, issues work otherwise. Individuals take part by default, and it is tougher to say what not collaborating is. You could possibly money out your R[i] and S[i] cash in trade for DAO tokens, however then if there is a want to try this then R[i] and S[i] can be undervalued and there can be an incentive to purchase each of them. Holding solely R[i] can also be not non-participating; it is really an expression of being bearish on the deserves of coverage P[i]; identical with holding solely S[i]. The truth is, the closest factor to a “default” technique is holding no matter R[i] and S[i] you get; we are able to mannequin this prediction market as a zero-supply market plus this additional preliminary allocation, so in that sense the “simply maintain” strategy is a default. Nonetheless, we are able to argue that the barrier to participation is way decrease, so participation will enhance.

Additionally notice that the optimization goal is less complicated; the futarchy isn’t making an attempt to mediate the principles of a whole authorities, it’s merely making an attempt to maximise the worth of its personal token by allocating a spending finances. Determining extra attention-grabbing optimization goals, maybe ones that penalize frequent dangerous acts carried out by current company entities, is an unsolved problem however an important one; at that time, the measurement and metric manipulation points may as soon as once more change into extra essential. Lastly, the precise day-to-day governance of the futarchy really does comply with a hybrid mannequin; the disbursements are made as soon as per epoch, however the administration of the funds inside that point could be left to people, centralized organizations, blockchain-based organizations or doubtlessly different DAOs. Thus, we are able to count on the variations in anticipated token worth between the proposals to be massive, so the futarchy really might be pretty efficient – or not less than simpler than the present most well-liked strategy of “5 builders resolve”.

Why?

So what are the sensible advantages of adopting such a scheme? What’s unsuitable with merely having blockchain-based organizations that comply with extra conventional fashions of governance, or much more democratic ones? Since most readers of this weblog are already cryptocurrency advocates, we are able to merely say that the explanation why that is the case is identical cause why we’re occupied with utilizing cryptographic protocols as a substitute of centrally managed techniques – cryptographic protocols have a a lot decrease want for trusting central authorities (if you’re not inclined to mistrust central authorities, the argument could be extra precisely rephrased as “cryptographic protocols can extra simply generalize to achieve the effectivity, fairness and informational advantages of being extra participatory and inclusive with out resulting in the consequence that you find yourself trusting unknown people”). So far as social penalties go, this easy model of futarchy is way from utopia, as it’s nonetheless pretty just like a profit-maximizing company; nevertheless, the 2 essential enhancements that it does make are (1) making it tougher for executives managing the funds to cheat each the group and society for his or her short-term curiosity, and (2) making governance radically open and clear.

Nonetheless, up till now, one of many main sore factors for a cryptographic protocol is how the protocol can fund and govern itself; the first answer, a centralized group with a one-time token issuance and presale, is principally a hack that generates preliminary funding and preliminary governance at the price of preliminary centralization. Token gross sales, together with our personal Ethereum ether sale, have been a controversial subject, to a big extent as a result of they introduce this blemish of centralization into what’s in any other case a pure and decentralized cryptosystem; nevertheless, if a brand new protocol begins off issuing itself as a futarchy from day one, then that protocol can obtain incentivization with out centralization – one of many key breakthroughs in economics that make the cryptocurrency house on the whole value watching.

Some could argue that inflationary token techniques are undesirable and that dilution is unhealthy; nevertheless, an essential level is that, if futarchy works, this scheme is assured to be not less than as efficient as a fixed-supply forex, and within the presence of a nonzero amount of doubtless satisfiable public items it will likely be strictly superior. The argument is straightforward: it’s all the time doable to give you a proposal that sends the funds to an unspendable handle, so any proposal that wins must win in opposition to that baseline as nicely.

So what are the primary protocols that we are going to see utilizing futarchy? Theoretically, any of the higher-level protocols which have their very own coin (eg. SWARM, StorJ, Maidsafe), however with out their very own blockchain, may benefit from futarchy on high of Ethereum. All that they would want to do is implement the futarchy in code (one thing which I have began to do already), add a reasonably person interface for the markets, and set it going. Though technically each single futarchy that begins off might be precisely the identical, futarchy is Schelling-point-dependent; in case you create a web site round one specific futarchy, label it “decentralized insurance coverage”, and collect a group round that concept, then it will likely be extra probably that that individual futarchy succeeds if it really follows by way of on the promise of decentralized insurance coverage, and so the market will favor proposals that truly have one thing to do with that individual line of improvement.

In case you are constructing a protocol that can have a blockchain however doesn’t but, then you need to use futarchy to handle a “protoshare” that can finally be transformed over; and if you’re constructing a protocol with a blockchain from the beginning you’ll be able to all the time embody futarchy proper into the core blockchain code itself; the one change might be that you’ll want to search out one thing to switch the usage of a “reference asset” (eg. 264 hashes may go as a trust-free financial unit of account). In fact, even on this kind futarchy can’t be assured to work; it’s only an experiment, and should nicely show inferior to different mechanisms like liquid democracy – or hybrid options could also be finest. However experiments are what cryptocurrency is all about.

from Ethereum – My Blog https://ift.tt/JS2I5HY

via IFTTT