Particular due to Robert Sams for the event of Seignorage Shares and insights relating to methods to accurately worth risky cash in multi-currency programs

Observe: we aren’t planning on including value stabilization to ether; our philosophy has all the time been to maintain ether easy to attenuate black-swan dangers. Outcomes of this analysis will seemingly go into both subcurrencies or unbiased blockchains

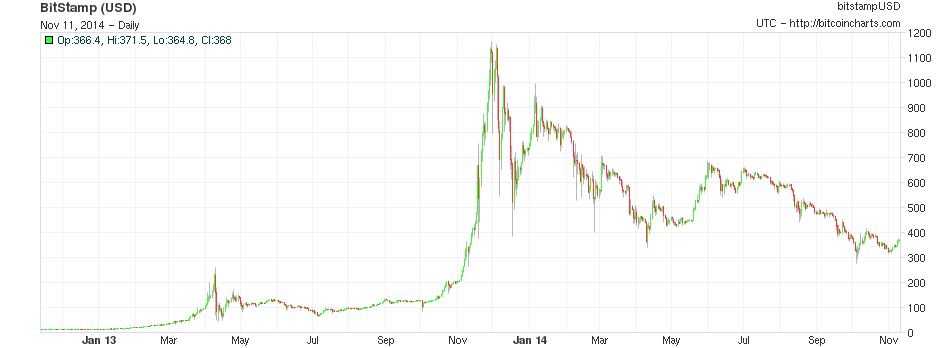

One of many essential issues with Bitcoin for bizarre customers is that, whereas the community could also be a good way of sending funds, with decrease transaction prices, far more expansive world attain, and a really excessive degree of censorship resistance, Bitcoin the foreign money is a really risky technique of storing worth. Though the foreign money had by and enormous grown by leaps and bounds over the previous six years, particularly in monetary markets previous efficiency is not any assure (and by environment friendly market speculation not even an indicator) of future outcomes of anticipated worth, and the foreign money additionally has a longtime fame for excessive volatility; over the previous eleven months, Bitcoin holders have misplaced about 67% of their wealth and very often the worth strikes up or down by as a lot as 25% in a single week. Seeing this concern, there’s a rising curiosity in a easy query: can we get the perfect of each worlds? Can now we have the total decentralization {that a} cryptographic fee community affords, however on the identical time have the next degree of value stability, with out such excessive upward and downward swings?

Final week, a crew of Japanese researchers made a proposal for an “improved Bitcoin”, which was an try and just do that: whereas Bitcoin has a hard and fast provide, and a risky value, the researchers’ Improved Bitcoin would fluctuate its provide in an try and mitigate the shocks in value. Nevertheless, the issue of creating a price-stable cryptocurrency, because the researchers realized, is way totally different from that of merely organising an inflation goal for a central financial institution. The underlying query is tougher: how will we goal a hard and fast value in a means that’s each decentralized and strong towards assault?

To resolve the problem correctly, it’s best to interrupt it down into two principally separate sub-problems:

- How will we measure a foreign money’s value in a decentralized means?

- Given a desired provide adjustment to focus on the worth, to whom will we subject and the way will we soak up foreign money models?

Decentralized Measurement

For the decentralized measurement drawback, there are two recognized main lessons of options: exogenous options, mechanisms which attempt to measure the worth with respect to some exact index from the surface, and endogenous options, mechanisms which attempt to use inner variables of the community to measure value. So far as exogenous options go, to this point the one dependable recognized class of mechanisms for (probably) cryptoeconomically securely figuring out the worth of an exogenous variable are the totally different variants of Schellingcoin – basically, have everybody vote on what the result’s (utilizing some set chosen randomly based mostly on mining energy or stake in some foreign money to forestall sybil assaults), and reward everybody that gives a consequence that’s near the bulk consensus. In the event you assume that everybody else will present correct info, then it’s in your curiosity to supply correct info with a purpose to be nearer to the consensus – a self-reinforcing mechanism very similar to cryptocurrency consensus itself.

The primary drawback with Schellingcoin is that it is not clear precisely how secure the consensus is. Significantly, what if some medium-sized actor pre-announces some various worth to the reality that will be helpful for many actors to undertake, and the actors handle to coordinate on switching over? If there was a big incentive, and if the pool of customers was comparatively centralized, it may not be too tough to coordinate on switching over.

There are three main components that may affect the extent of this vulnerability:

- Is it seemingly that the individuals in a schellingcoin even have a standard incentive to bias the end in some route?

- Do the individuals have some widespread stake within the system that will be devalued if the system had been to be dishonest?

- Is it doable to “credibly commit” to a specific reply (ie. decide to offering the reply in a means that clearly cannot be modified)?

(1) is slightly problematic for single-currency programs, as if the set of individuals is chosen by their stake within the foreign money then they’ve a robust incentive to faux the foreign money value is decrease in order that the compensation mechanism will push it up, and if the set of individuals is chosen by mining energy then they’ve a robust incentive to faux the foreign money’s value is just too excessive in order to extend the issuance. Now, if there are two sorts of mining, one in every of which is used to pick Schellingcoin individuals and the opposite to obtain a variable reward, then this objection now not applies, and multi-currency programs may also get round the issue. (2) is true if the participant choice relies on both stake (ideally, long-term bonded stake) or ASIC mining, however false for CPU mining. Nevertheless, we should always not merely depend on this incentive to outweigh (1).

(3) is probably the toughest; it is determined by the exact technical implementation of the Schellingcoin. A easy implementation involving merely submitting the values to the blockchain is problematic as a result of merely submitting one’s worth early is a reputable dedication. The unique SchellingCoin used a mechanism of getting everybody submit a hash of the worth within the first spherical, and the precise worth within the second spherical, type of a cryptographic equal to requiring everybody to place down a card face down first, after which flip it on the identical time; nonetheless, this too permits credible dedication by revealing (even when not submitting) one’s worth early, as the worth could be checked towards the hash.

A 3rd choice is requiring the entire individuals to submit their values immediately, however solely throughout a selected block; if a participant does launch a submission early they will all the time “double-spend” it. The 12-second block time would imply that there’s nearly no time for coordination. The creator of the block could be strongly incentivized (and even, if the Schellingcoin is an unbiased blockchain, required) to incorporate all participations, to discourage or stop the block maker from selecting and selecting solutions. A fourth class of choices includes some secret sharing or safe multiparty computation mechanism, utilizing a set of nodes, themselves chosen by stake (even perhaps the individuals themselves), as a type of decentralized substitute for a centralized server answer, with all of the privateness that such an method entails.

Lastly, a fifth technique is to do the schellingcoin “blockchain-style”: each interval, some random stakeholder is chosen, and instructed to supply their vote as a [id, value] pair, the place worth is the precise legitimate and id is an identifier of the earlier vote that appears appropriate. The inducement to vote accurately is that solely checks that stay in the principle chain after some variety of blocks are rewarded, and future voters will notice connect their vote to a vote that’s incorrect fearing that in the event that they do voters after them will reject their vote.

Schellingcoin is an untested experiment, and so there’s reputable motive to be skeptical that it’ll work; nonetheless, if we wish something near an ideal value measurement scheme it is at present the one mechanism that now we have. If Schellingcoin proves unworkable, then we should make do with the opposite sorts of methods: the endogenous ones.

Endogenous Options

To measure the worth of a foreign money endogenously, what we basically want is to seek out some service contained in the community that’s recognized to have a roughly secure real-value value, and measure the worth of that service contained in the community as measured within the community’s personal token. Examples of such providers embrace:

- Computation (measured through mining problem)

- Transaction charges

- Information storage

- Bandwidth provision

A barely totally different, however associated, technique, is to measure some statistic that correllates not directly with value, normally a metric of the extent of utilization; one instance of that is transaction quantity.

The issue with all of those providers is, nonetheless, that none of them are very strong towards speedy modifications attributable to technological innovation. Moore’s Legislation has to this point assured that the majority types of computational providers develop into cheaper at a charge of 2x each two years, and it may simply pace as much as 2x each 18 months or 2x each 5 years. Therefore, making an attempt to peg a foreign money to any of these variables will seemingly result in a system which is hyperinflationary, and so we’d like some extra superior methods for utilizing these variables to find out a extra secure metric of the worth.

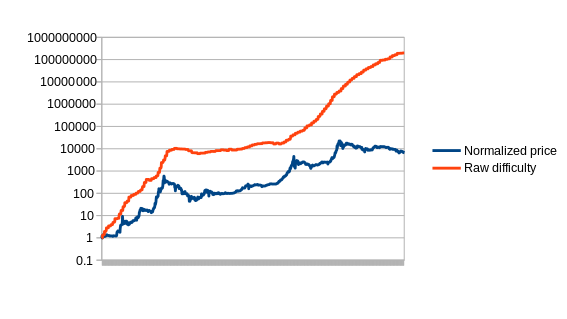

First, allow us to arrange the issue. Formally, we outline an estimator to be a operate which receives an information feed of some enter variable (eg. mining problem, transaction price in foreign money models, and so on) D[1], D[2], D[3]…, and must output a stream of estimates of the foreign money’s value, P[1], P[2], P[3]… The estimator clearly can’t look into the longer term; P[i] could be depending on D[1], D[2] … D[i], however not D[i+1]. Now, to start out off, allow us to graph the best doable estimator on Bitcoin, which we’ll name the naive estimator: problem equals value.

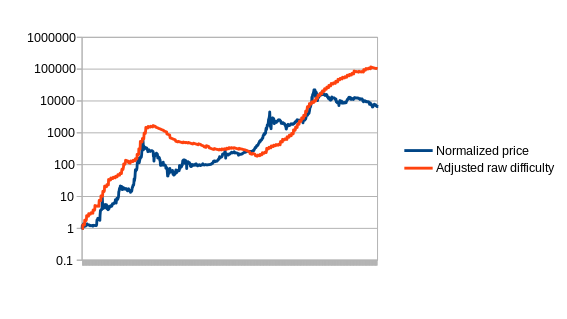

Sadly, the issue with this method is apparent from the graph and was already talked about above: problem is a operate of each value and Moore’s regulation, and so it offers outcomes that depart from any correct measure of the worth exponentially over time. The primary speedy technique to repair this drawback is to attempt to compensate for Moore’s regulation, utilizing the issue however artificially lowering the worth by some fixed per day to counteract the anticipated pace of technological progress; we’ll name this the compensated naive estimator. Observe that there are an infinite variety of variations of this estimator, one for every depreciation charge, and the entire different estimators that we present right here will even have parameters.

The best way that we are going to choose the parameter for our model is through the use of a variant of simulated annealing to seek out the optimum values, utilizing the primary 780 days of the Bitcoin value as “coaching information”. The estimators are then left to carry out as they’d for the remaining 780 days, to see how they’d react to circumstances that had been unknown when the parameters had been optimized (this system, is aware of as “cross-validation”, is customary in machine studying and optimization idea). The optimum worth for the compensated estimator is a drop of 0.48% per day, resulting in this chart:

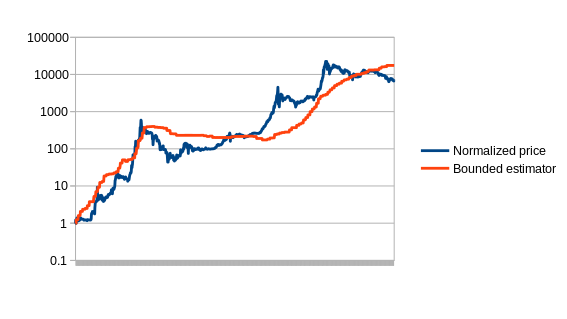

The following estimator that we are going to discover is the bounded estimator. The best way the bounded estimator works is considerably extra sophisticated. By default, it assumes that every one development in problem is because of Moore’s regulation. Nevertheless, it assumes that Moore’s regulation can’t go backwards (ie. know-how getting worse), and that Moore’s regulation can’t go quicker than some charge – within the case of our model, 5.88% per two weeks, or roughly quadrupling yearly. Any development exterior these bounds it assumes is coming from value rises or drops. Thus, for instance, if the issue rises by 20% in a single interval, it assumes that 5.88% of it is because of technological developments, and the remaining 14.12% is because of a value improve, and thus a stabilizing foreign money based mostly on this estimator would possibly improve provide by 14.12% to compensate. The idea is that cryptocurrency value development to a big extent occurs in speedy bubbles, and thus the bounded estimator ought to have the ability to seize the majority of the worth development throughout such occasions.

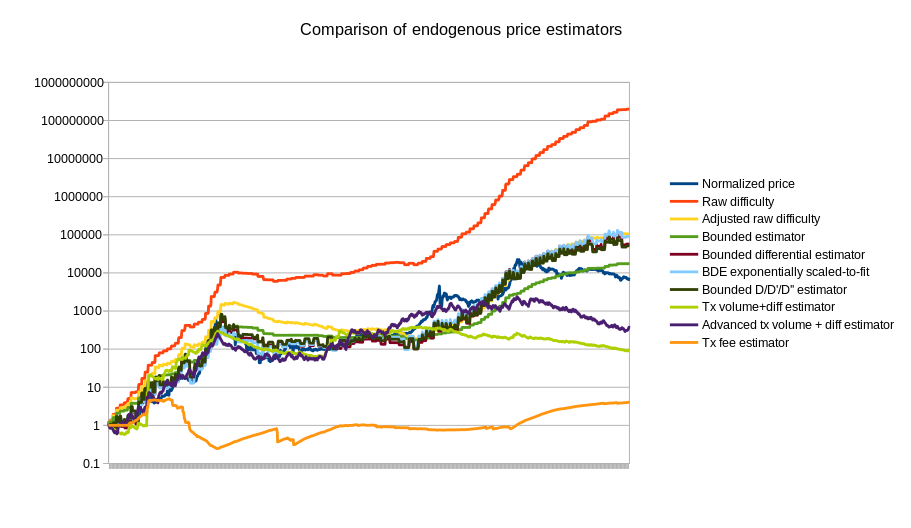

There are extra superior methods as nicely; the perfect methods ought to keep in mind the truth that ASIC farms take time to arrange, and likewise observe a hysteresis impact: it is typically viable to maintain an ASIC farm on-line if you have already got it even when underneath the identical circumstances it will not be viable to start out up a brand new one. A easy method is trying on the charge of improve of the issue, and never simply the issue itself, and even utilizing a linear regression evaluation to undertaking problem 90 days into the longer term. Here’s a chart containing the above estimators, plus a couple of others, in comparison with the precise value:

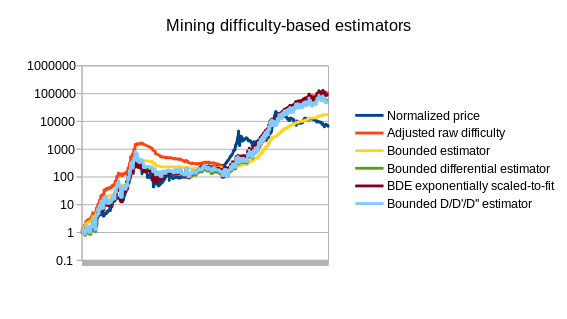

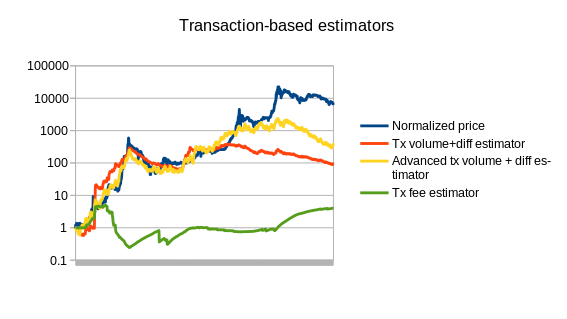

Observe that the chart additionally consists of three estimators that use statistics aside from Bitcoin mining: a easy and a sophisticated estimator utilizing transaction quantity, and an estimator utilizing the common transaction payment. We are able to additionally cut up up the mining-based estimators from the opposite estimators:

|

|

See https://ift.tt/3I7cgQB for the supply code that produced these outcomes.

In fact, that is solely the start of endogenous value estimator idea; a extra thorough evaluation involving dozens of cryptocurrencies will seemingly go a lot additional. The most effective estimators might nicely find yourself utilizing a mix of various measures; seeing how the difficulty-based estimators overshot the worth in 2014 and the transaction-based estimators undershot the worth, the 2 mixed may find yourself being considerably extra correct. The issue can also be going to get simpler over time as we see the Bitcoin mining economic system stabilize towards one thing nearer to an equilibrium the place know-how improves solely as quick as the final Moore’s regulation rule of 2x each 2 years.

To see simply how good these estimators can get, we are able to notice from the charts that they will cancel out a minimum of 50% of cryptocurrency value volatility, and will improve to ~67% as soon as the mining business stabilizes. One thing like Bitcoin, if it turns into mainstream, will seemingly be considerably extra unstable than gold, however not that rather more unstable – the one distinction between BTC and gold is that the provision of gold can really improve as the worth goes greater since extra could be mined if miners are prepared to pay greater prices, so there’s an implicit dampening impact, however the provide elasticity of gold is surprisingly not that excessive; manufacturing barely elevated in any respect throughout the run-ups in value throughout the Seventies and 2000s. The value of gold stayed inside a variety of 4.63x ($412 to $1980) within the final decade; logarithmically lowering that by two thirds offers a variety of 1.54x, not a lot greater than EUR/USD (1.37x), JPY/USD (1.64x) or CAD/USD (1.41x); thus, endogenous stabilization might nicely show fairly viable, and could also be most popular attributable to its lack of tie to any particular centralized foreign money or authority.

The opposite subject that every one of those estimators must take care of is exploitability: if transaction quantity is used to find out the foreign money’s value, then an attacker can manipulate the worth very simply by merely sending very many transactions. The common transaction charges paid in Bitcoin are about $5000 per day; at that value in a stabilized foreign money the attacker would have the ability to halve the worth. Mining problem, nonetheless, is far more tough to use just because the market is so giant. If a platform doesn’t wish to settle for the inefficiencies of wasteful proof of labor, an alternate is to construct in a marketplace for different assets, resembling storage, as an alternative; Filecoin and Permacoin are two efforts that try to make use of a decentralized file storage market as a consensus mechanism, and the identical market may simply be dual-purposed to function an estimator.

The Issuance Drawback

Now, even when now we have a fairly good, and even good, estimator for the foreign money’s value, we nonetheless have the second drawback: how will we subject or soak up foreign money models? The only method is to easily subject them as a mining reward, as proposed by the Japanese researchers. Nevertheless, this has two issues:

- Such a mechanism can solely subject new foreign money models when the worth is just too excessive; it can’t soak up foreign money models when the worth is just too low.

- If we’re utilizing mining problem in an endogenous estimator, then the estimator must keep in mind the truth that a number of the will increase in mining problem will likely be a results of an elevated issuance charge triggered by the estimator itself.

If not dealt with very fastidiously, the second drawback has the potential to create some slightly harmful suggestions loops in both route; nonetheless, if we use a unique market as an estimator and as an issuance mannequin then this is not going to be an issue. The primary drawback appears severe; in actual fact, one can interpret it as saying that any foreign money utilizing this mannequin will all the time be strictly worse than Bitcoin, as a result of Bitcoin will ultimately have an issuance charge of zero and a foreign money utilizing this mechanism could have an issuance charge all the time above zero. Therefore, the foreign money will all the time be extra inflationary, and thus much less enticing to carry. Nevertheless, this argument isn’t fairly true; the reason being that when a person purchases models of the stabilized foreign money then they’ve extra confidence that on the time of buy the models aren’t already overvalued and subsequently will quickly decline. Alternatively, one can notice that extraordinarily giant swings in value are justified by altering estimations of the chance the foreign money will develop into 1000’s of instances costlier; clipping off this risk will cut back the upward and downward extent of those swings. For customers who care about stability, this danger discount might nicely outweigh the elevated normal long-term provide inflation.

BitAssets

A second method is the (unique implementation of the) “bitassets” technique utilized by Bitshares. This method could be described as follows:

- There exist two currencies, “vol-coins” and “stable-coins”.

- Secure-coins are understood to have a price of $1.

- Vol-coins are an precise foreign money; customers can have a zero or constructive stability of them. Secure-coins exist solely within the type of contracts-for-difference (ie. each detrimental stable-coin is known as a debt to another person, collateralized by a minimum of 2x the worth in vol-coins, and each constructive stable-coin is the possession of that debt).

- If the worth of somebody’s stable-coin debt exceeds 90% of the worth of their vol-coin collateral, the debt is cancelled and the whole vol-coin collateral is transferred to the counterparty (“margin name”)

- Customers are free to commerce vol-coins and stable-coins with one another.

And that is it. The important thing piece that makes the mechanism (supposedly) work is the idea of a “market peg”: as a result of everybody understands that stable-coins are purported to be price $1, if the worth of a stable-coin drops beneath $1, then everybody will notice that it’ll ultimately return to $1, and so folks will purchase it, so it really will return to $1 – a self-fulfilling prophecy argument. And for the same motive, if the worth goes above $1, it would return down. As a result of stable-coins are a zero-total-supply foreign money (ie. every constructive unit is matched by a corresponding detrimental unit), the mechanism isn’t intrinsically unworkable; a value of $1 might be secure with ten customers or ten billion customers (bear in mind, fridges are customers too!).

Nevertheless, the mechanism has some slightly severe fragility properties. Certain, if the worth of a stable-coin goes to $0.95, and it is a small drop that may simply be corrected, then the mechanism will come into play, and the worth will shortly return to $1. Nevertheless, if the worth immediately drops to $0.90, or decrease, then customers might interpret the drop as an indication that the peg is definitely breaking, and can begin scrambling to get out whereas they will – thus making the worth fall even additional. On the finish, the stable-coin may simply find yourself being price nothing in any respect. In the true world, markets do typically present constructive suggestions loops, and it’s fairly seemingly that the one motive the system has not fallen aside already is as a result of everybody is aware of that there exists a big centralized group (BitShares Inc) which is prepared to behave as a purchaser of final resort to take care of the “market” peg if vital.

Observe that BitShares has now moved to a considerably totally different mannequin involving value feeds offered by the delegates (individuals within the consensus algorithm) of the system; therefore the fragility dangers are seemingly considerably decrease now.

SchellingDollar

An method vaguely much like BitAssets that arguably works significantly better is the SchellingDollar (known as that means as a result of it was initially supposed to work with the SchellingCoin value detection mechanism, but it surely may also be used with endogenous estimators), outlined as follows:

- There exist two currencies, “vol-coins” and “stable-coins”. Vol-coins are initially distributed one way or the other (eg. pre-sale), however initially no stable-coins exist.

- Customers might have solely a zero or constructive stability of vol-coins. Customers might have a detrimental stability of stable-coins, however can solely purchase or improve their detrimental stability of stable-coins if they’ve a amount of vol-coins equal in worth to twice their new stable-coin stability (eg. if a stable-coin is $1 and a vol-coin is $5, then if a person has 10 vol-coins ($50) they will at most cut back their stable-coin stability to -25)

- If the worth of a person’s detrimental stable-coins exceeds 90% of the worth of the person’s vol-coins, then the person’s stable-coin and vol-coin balances are each diminished to zero (“margin name”). This prevents conditions the place accounts exist with negative-valued balances and the system goes bankrupt as customers run away from their debt.

- Customers can convert their stable-coins into vol-coins or their vol-coins into stable-coins at a charge of $1 price of vol-coin per stable-coin, maybe with a 0.1% alternate payment. This mechanism is in fact topic to the bounds described in (2).

- The system retains monitor of the overall amount of stable-coins in circulation. If the amount exceeds zero, the system imposes a detrimental rate of interest to make constructive stable-coin holdings much less enticing and detrimental holdings extra enticing. If the amount is lower than zero, the system equally imposes a constructive rate of interest. Rates of interest could be adjusted through one thing like a PID controller, or perhaps a easy “improve or lower by 0.2% day by day based mostly on whether or not the amount is constructive or detrimental” rule.

Right here, we don’t merely assume that the market will preserve the worth at $1; as an alternative, we use a central-bank-style rate of interest focusing on mechanism to artificially discourage holding stable-coin models if the provision is just too excessive (ie. larger than zero), and encourage holding stable-coin models if the provision is just too low (ie. lower than zero). Observe that there are nonetheless fragility dangers right here. First, if the vol-coin value falls by greater than 50% in a short time, then many margin name circumstances will likely be triggered, drastically shifting the stable-coin provide to the constructive facet, and thus forcing a excessive detrimental rate of interest on stable-coins. Second, if the vol-coin market is just too skinny, then it will likely be simply manipulable, permitting attackers to set off margin name cascades.

One other concern is, why would vol-coins be worthwhile? Shortage alone is not going to present a lot worth, since vol-coins are inferior to stable-coins for transactional functions. We are able to see the reply by modeling the system as a type of decentralized company, the place “making earnings” is equal to absorbing vol-coins and “taking losses” is equal to issuing vol-coins. The system’s revenue and loss eventualities are as follows:

- Revenue: transaction charges from exchanging stable-coins for vol-coins

- Revenue: the additional 10% in margin name conditions

- Loss: conditions the place the vol-coin value falls whereas the overall stable-coin provide is constructive, or rises whereas the overall stable-coin provide is detrimental (the primary case is extra more likely to occur, attributable to margin-call conditions)

- Revenue: conditions the place the vol-coin value rises whereas the overall stable-coin provide is constructive, or falls whereas it is detrimental

Observe that the second revenue is in some methods a phantom revenue; when customers maintain vol-coins, they might want to keep in mind the chance that they are going to be on the receiving finish of this further 10% seizure, which cancels out the profit to the system from the revenue present. Nevertheless, one would possibly argue that due to the Dunning-Kruger impact customers would possibly underestimate their susceptibility to consuming the loss, and thus the compensation will likely be lower than 100%.

Now, take into account a technique the place a person tries to carry on to a relentless share of all vol-coins. When x% of vol-coins are absorbed, the person sells off x% of their vol-coins and takes a revenue, and when new vol-coins equal to x% of the present provide are launched, the person will increase their holdings by the identical portion, taking a loss. Thus, the person’s web revenue is proportional to the overall revenue of the system.

Seignorage Shares

A fourth mannequin is “seignorage shares”, courtesy of Robert Sams. Seignorage shares is a slightly elegant scheme that, in my very own simplified tackle the scheme, works as follows:

- There exist two currencies, “vol-coins” and “stable-coins” (Sams makes use of “shares” and “cash”, respectively)

- Anybody should buy vol-coins for stable-coins or vol-coins for stable-coins from the system at a charge of $1 price of vol-coin per stable-coin, maybe with a 0.1% alternate payment

Observe that in Sams’ model, an public sale was used to unload newly-created stable-coins if the worth goes too excessive, and purchase if it goes too low; this mechanism mainly has the identical impact, besides utilizing an always-available mounted value rather than an public sale. Nevertheless, the simplicity comes at the price of a point of fragility. To see why, allow us to make an identical valuation evaluation for vol-coins. The revenue and loss eventualities are easy:

- Revenue: absorbing vol-coins to subject new stable-coins

- Loss: issuing vol-coins to soak up stable-coins

The identical valuation technique applies as within the different case, so we are able to see that the worth of the vol-coins is proportional to the anticipated whole future improve within the provide of stable-coins, adjusted by some discounting issue. Thus, right here lies the issue: if the system is known by all events to be “winding down” (eg. customers are abandoning it for a superior competitor), and thus the overall stable-coin provide is predicted to go down and by no means come again up, then the worth of the vol-coins drops beneath zero, so vol-coins hyperinflate, after which stable-coins hyperinflate. In alternate for this fragility danger, nonetheless, vol-coins can obtain a a lot greater valuation, so the scheme is far more enticing to cryptoplatform builders seeking to earn income through a token sale.

Observe that each the SchellingDollar and seignorage shares, if they’re on an unbiased community, additionally must keep in mind transaction charges and consensus prices. Thankfully, with proof of stake, it ought to be doable to make consensus cheaper than transaction charges, wherein case the distinction could be added to earnings. This doubtlessly permits for a bigger market cap for the SchellingDollar’s vol-coin, and permits the market cap of seignorage shares’ vol-coins to stay above zero even within the occasion of a considerable, albeit not whole, everlasting lower in stable-coin quantity. In the end, nonetheless, a point of fragility is inevitable: on the very least, if curiosity in a system drops to near-zero, then the system could be double-spent and estimators and Schellingcoins exploited to loss of life. Even sidechains, as a scheme for preserving one foreign money throughout a number of networks, are inclined to this drawback. The query is solely (1) how will we reduce the dangers, and (2) provided that dangers exist, how will we current the system to customers in order that they don’t develop into overly depending on one thing that would break?

Conclusions

Are stable-value belongings vital? Given the excessive degree of curiosity in “blockchain know-how” coupled with disinterest in “Bitcoin the foreign money” that we see amongst so many within the mainstream world, maybe the time is ripe for stable-currency or multi-currency programs to take over. There would then be a number of separate lessons of cryptoassets: secure belongings for buying and selling, speculative belongings for funding, and Bitcoin itself might nicely function a singular Schelling level for a common fallback asset, much like the present and historic functioning of gold.

If that had been to occur, and significantly if the stronger model of value stability based mostly on Schellingcoin methods may take off, the cryptocurrency panorama might find yourself in an fascinating scenario: there could also be 1000’s of cryptocurrencies, of which many can be risky, however many others can be stable-coins, all adjusting costs practically in lockstep with one another; therefore, the scenario may even find yourself being expressed in interfaces as a single super-currency, however the place totally different blockchains randomly give constructive or detrimental rates of interest, very similar to Ferdinando Ametrano’s “Hayek Cash”. The true cryptoeconomy of the longer term might haven’t even begun to take form.

from Ethereum – My Blog https://ift.tt/9PwpNVZ

via IFTTT